If a segment of the company iseliminated, the indirect cost for depreciation assigned to thatsegment does not disappear; the cost is simply allocated among theremaining segments. In a given situation, it may be possible toidentify an indirect cost that would be eliminated if the costobject were eliminated, but this would be the exception to thegeneral rule. Contribution margin and regular income statements can be very detailed, requiring an in-depth understanding of the business’s inner workings. Looking at the variable expenses, each skincare product needs ingredients to be formulated, some nice packaging, and a good salesperson on commission. Investors examine contribution margins to determine if a company is using its revenue effectively. A high contribution margin indicates that a company tends to bring in more money than it spends.

4: The Contribution Margin Income Statement

To understand segmental analysis, you need toknow about the concepts of variable cost, fixed cost, direct cost,indirect cost, net income of a segment, and contribution toindirect expenses. Some common examples of variable costs are raw materials, packaging, and the labor cost of making the product. In its simplest form, a contribution margin is the price of a specific product minus the variable costs of producing the item. What’s left is the contribution margin, which gives a sense of how much is left over to cover fixed expenses and make a profit. Using this contribution margin format makes it easy to see the impact of changing sales volume on operating income.

Formula and Calculation of Contribution Margin

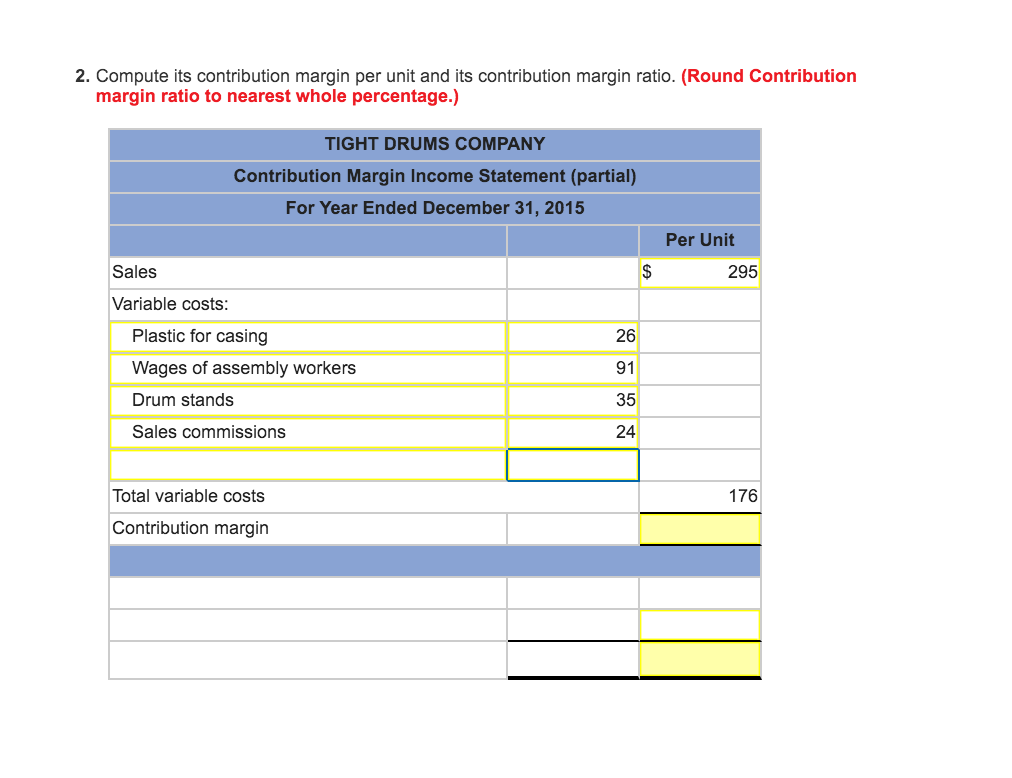

Regardless of how contribution margin is expressed, it provides critical information for managers. Understanding how each product, good, or service contributes to the organization’s profitability allows managers to make decisions such as which product lines they should expand or which might be discontinued. When allocating scarce resources, the contribution margin will help them focus on those products or services with the highest margin, thereby maximizing profits. In May, \(750\) of the Blue Jay models were sold as shown on the contribution margin income statement.

Contribution Margin Ratio

ABC Cabinets can use the contribution format for segment analysis, evaluating its two business segments and their relative contribution margins. Managers would have to determine the allocation of variable and fixed costs to each segment. You might wonder why a company would trade variable costs for fixed costs. One reason might be to meet company goals, such as gaining market share. Other reasons include being a leader in the use of innovation and improving efficiencies.

Since machine and software costs are often depreciated or amortized, these costs tend to be the same or fixed, no matter the level of activity within a given relevant range. Recall that Building Blocks of Managerial Accounting explained the characteristics of fixed and variable costs and introduced the basics of cost behavior. The company will use this “margin” to cover fixed expenses and hopefully to provide a profit.

Sales Revenue

- You’ll notice that the above statement doesn’t include the contribution margin.

- Costs may be either directly or indirectlyrelated to a particular cost object.

- The same thing goes with fixed expenses; they must be included in fixed costs if they are fixed.

- Investors examine contribution margins to determine if a company is using its revenue effectively.

- For certain other indirect expenses, accountantsbase allocation on responsibility for incurrence.

Every dollar of revenue generated goes into Contribution Margin or Variable Costs. What’s left in the contribution margin covers Fixed Costs and remains in the Net Profit / Loss. The IRA catch‑up contribution limit for individuals aged 50 and over was amended under the SECURE 2.0 Act of 2022 (SECURE 2.0) to include an annual cost‑of‑living adjustment but remains $1,000 for 2025. 2020 review of xero practice manager WASHINGTON — The Internal Revenue Service announced today that the amount individuals can contribute to their 401(k) plans in 2025 has increased to $23,500, up from $23,000 for 2024. Going back to that beauty company example from earlier, we’ll assume the business has expanded into the high-end skincare market and wants to see how the new line is performing financially.

Variable costs, no matter if they are product or period costs appear at the top of the statement. It is helpful to calculate the variable product cost before starting, especially if you will need to calculate ending inventory. Along with the company management, vigilant investors may keep a close eye on the contribution margin of a high-performing product relative to other products in order to assess the company’s dependence on its star performer. Fixed costs are often considered sunk costs that once spent cannot be recovered. These cost components should not be considered while making decisions about cost analysis or profitability measures. Parties concerned with the financial aspects of the business may be more likely to understand break-even in dollars; someone interested in operations may be more concerned with break-even in units.

Let’s examine how all three approaches convey the same financial performance, although represented somewhat differently. The difference between fixed and variable costs has to do with their correlation to the production levels of a company. As we said earlier, variable costs have a direct relationship with production levels.

Fixed expenses are then subtracted to arrive at the net profit or loss for the period. You can’t directly calculate the contribution margin from the EBIT figure, without a breakdown of the fixed and variable costs for each product or service. A contribution margin is a gap between the revenue of a product and the variable costs it took to make it. Earnings Before Interest and Taxes (EBIT) is the company’s net income before applying taxes and interest rates.

Direct materials are often typical variable costs, because you normally use more direct materials when you produce more items. In our example, if the students sold \(100\) shirts, assuming an individual variable cost per shirt of \(\$10\), the total variable costs would be \(\$1,000\) (\(100 × \$10\)). If they sold \(250\) shirts, again assuming an individual variable cost per shirt of \(\$10\), then the total variable costs would \(\$2,500 (250 × \$10)\). A contribution margin income statement, on the other hand, is a purely management oriented format of presenting revenues and expenses that helps in various revenues and expense related decision making processes. For example, a multi-product company can measure profitability of each product by preparing a product viz contribution margin income statement and decide which product to continue and which one to drop.